|

I've never before posted something that was too big for AtomicBobs . . . but this one apparently did the trick. So I broke the post into five parts - which may be more palatable for the average reader anyway! And it seems to be working...

Saturday, April 23, 2011

Deflation or Hyperinflation?

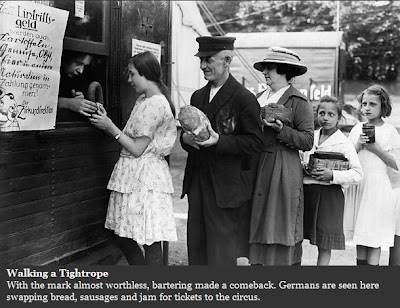

Chapter 84 â Bond salesmen's propaganda that "a dollar is a dollar" should be rewritten to say "a dollar is 3¢"

Since most ordinary people, bankers, and company presidents have never studied currency theory, they swallow it hook, line, and sinker when the bond salesmen tell them, "a dollar is a dollar." That piece of propaganda should be rewritten to say "a dollar is 3¢." The nominal dollar is officially worth no more than 14¢ of its 1940 value, unofficially only 3¢.

If computed in 1940 constant dollars, not more than $1,380 exists of the US $46,000 per capita gross public and private debt. More than $44,628 has been destroyed by inflation. But sadly, the owners of this debt do not want to hear about it. They do not wish to know that bonds are issued by governments with the sole purpose of debasement.

To my knowledge, no government in history has paid its debts in currency equal to the purchasing power of the currency lent to them. The people always lose their money on bonds.

It angers me. Bond salesmen should be thrown into the East River.

-The above was written in 1985 by Dr. Franz Pick, in the book "The Triumph of Gold" sent to me by one of my readers. The photos are from Time Magazine.

The whole point of the deflation versus hyperinflation debate is about the denouement, the final outcome of this 100-year dollar experiment. It is about the ultimate end, and the debate has been going on ever since the 70s when the dollar was separated from gold and it became clear that there would be an end. The debate is about determining the best stance someone should take who has plenty of net worth. And I do mean PLENTY. People of modest net worth, like me, can of course participate in the debate. But then it can become confusing at times when we think about shortages or supply disruptions of necessities like food. Of course you need to look out for life's necessities first and foremost. But beyond that, there is real value to be gained by truly understanding this debate.

I want to apologize in advance for the length of this post, but I have to be thorough if I want to have any chance of winning Rick Ackerman over to the hyperinflation/Freegold side. And I think there is a chance. While deflation and inflation are practically polar opposites, deflation and hyperinflation look almost identical on the surface, with the main difference being the wheelbarrows of worthless cash. As I wrote in 2009 in The Waterfall Effect:

There is a quote I like that comes from Le Metropole Cafe. It goes, "we will have deflation in everything we own, and inflation in everything we use". This is partly true. It is true during the run up to the rubber band snapping. It is true until we hit the waterfall. At that point I have my own version of the quote. "We will have hyperDEflation in everything measured against real money, GOLD, and we will have hyperINflation in everything measured against paper dollars."

My latest post on this subject was called Big Gap in Understanding Weakens Deflationist Argument in response to Rick Ackerman's "Big Gap in Logic Weakens Hyperinflation Argument". Rick also received responses from Jim Willie and Gonzalo Lira. Last week, with regard to Lira and Willie, Rick reported to his readers in "Rick's Picks":

Iâve concluded there is little to gain arguing on the one hand with a guy who turns rabid whenever someone contradicts him, even in a friendly way; and on the other, with a preening narcissist who comes to argumentation in the same state of sexual arousal that Jeffrey Dahmer must have experienced hovering over the fresh corpses of teenage boys. These guys are bad news, as lacking in civility and manners as buzzards in a scrum, and youâd do well to avoid them both. You might try tuning instead to the hyperinflation arguments of Steve Saville, Peter Schiff and a few others who seem less concerned with trouncing, slicing and dicing opponents than with presenting facts that might better prepare you for the financial crisis ahead. The very best of them, in my opinion, is FOFOA blogspot, where the essays are erudite, the discussion elevated and the arguments as knowledgeable as any you will find on the web.

I would first like to thank Rick Ackerman, and to also acknowledge his perspicacity in this particular regard. And because he has demonstrated such a discerning acumen in his preference for hyperinflationists (among other things), I will try, once again, to help him see the way. As our own Blondie likes to say (and I paraphrase for clarity), "you don't own your baggage, it owns you." Here is Rick's baggage, in his own words:

My instincts concerning deflation were hard-wired in 1976 after reading C.V. Myersâ The Coming Deflation. The title was premature, as we now know, but the bookâs core idea was as timeless and immutable as the Law of Gravity. Myers stated, with elegant simplicity, that âUltimately, every penny of every debt must be paid â if not by the borrower, then by the lender.â Inflationists and deflationists implicitly agree on this point â we are all ruinists at heart, as our readers will long since have surmised, and we differ only on the question of who, borrower or lender, will take the hit. As Myers made clear, however, someone will have to pay. If you understand this, then you understand why the dreadnought of real estate deflation, for one, will remain with us even if 30 million terminally afflicted homeowners leave their house keys in the mailbox. To repeat: We do not make debt disappear by walking away from it; someone will have to take the hit.

Rick repeats what he calls "C.V. Myers' dictum" quite often in his deflation-oriented posts: âUltimately, every penny of every debt must be paid â if not by the borrower, then by the lender.â I'm going to go out on a limb here and say that this dictum is Rick's baggage, his foundational deflation premise, in a nutshell. And it leads him to his "bottom line" or his analytical conclusion:

Rick's Picks Commenter SD1: To my knowledge, no bank has ever made provisions in their lending criteria. So to anyone subscribing to the hyperinflation theory, all I can say is there is nothing I, and millions of other North Americans, would love more than to take $250,000 of worthless, hyperinflated money that we worked a few days to make, to pay off a mortgage that would otherwise have taken twenty-five to thirty years to repay.

Rick Ackerman:Thatâs the bottom line, as far as Iâm concerned.

In this post I will explain the flaw in Myers' dictum. I will go into great detail as to why the missing component in the dictum is the essential (and inevitable) one. I will show how this one flaw in Rick's premise sends his otherwise excellent analysis careening 180 degrees in the wrong direction (with regard to the subject of this post). And I will explain the proper frame of reference from which to view what I am describing. How's that for a kick-off?

First Myers' dictum. âUltimately, every penny of every debt must be paid â if not by the borrower, then by the lender.â Rick: "Inflationists and deflationists implicitly agree on this point â we are all ruinists at heart, as our readers will long since have surmised, and we differ only on the question of who, borrower or lender, will take the hit." Me: Yes, someone will pay. But there is a third option that is missing from Myers' dictum. "The hit" can be socialized:

"Human nature has followed this path for thousands of years. You know the old joke about outrunning the bear? Well, these lenders will influence our financial policy as such. They will try to get their debt securities liquefied first, spend the fiat and in this process outrun you and I. Leaving anyone they can beat to the mercy of the hyperinflation bear eating their remaining fiat assetsâ¦"

"â¦hyperinflation is the process of saving debt at all costs, even buying it outright for cash⦠because policy will allow the printing of cash, if necessary, to cover every last bit of debt and dumping it on your front lawn!"

(The quotes are from FOA on Hyperinflation and FOA on Currency Styling, Currency Management, Dollar Hyperinflation and End Game Scenarios respectively.)

As many of you know, I came to this debate, with no baggage and no hard opinion, in 2008. And in the "doom and gloom internet community" where I arrived there was definitely an equal helping of both deflation and inflation/hyperinflation talk. Most of it I found less than convincing (on both sides). The "deflation side" is actually bigger than you might think. Most of the peak this or peak that crowd, the majority of the survivalist community, and the Great American Collapse people are all expecting a sort of grand deflation, whether they understand the arguments or not.

If you want to think of a grand deflation as a deflatingâor grand contractionâof economic activity that was previously "energized" by massive trade deficits, massive credit expansion, and the massive structural malinvestment that flows from those easy money expansions, well then I too am expecting a sort of grand deflation, in many of the same ways they are. But one thing I have learned from the writer that made the most sense to me, the writer that I found most convincing from within my "past baggage" vacuum, is that "deflationists" as a group still have a big gap in understanding.

Rick became a deflationist in the 1970s by his own account. And he certainly wasn't alone. I wasn't even aware of the existence of such a debate in the 1970s let alone 2007, so I can hardly add the wide perspective necessary in this debate from my own personal experience. What I can do, instead, is to share with you this excerpt from the one that spoke convincingly to me, the one that informed my developing view in 2008.

One point I hope you'll find curious in this excerpt is that deflationists have always fixated on residential real estate. This is one of Rick Ackerman's, almost obsessive, objections to the hyperinflation case, and it clearly has roots in his kind. This was written in 2001, just as the housing bubble was developing. My notes in [brackets]:

Somewhere in the 1970s era I was exposed to the thinking of several different deflationists. It seemed that all of their conclusions came to the same end: that dollar deflation would rule the day, no matter what. Mind you now,,,,,, most of them were split on the finer points of the issue, but for all of them; [de]flation would have its day even if prices would rise somewhat. Deflation was always the final outcome.

One of the central themes in these thoughts was concerning how this coming deflation would impact plain old residential real estate. You see, most of these guys advocated selling excess residential property because it was, sooner or later, going down for the count. Mostly because the mortgage markets would be destroyed in the deflation and nobody could buy [prices would collapse to the cash price].

-- Note: The reader has to understand that these discussions were directed towards people and investors that had plenty of net worth. And I do mean Plenty! The argument wasn't about how to survive; rather how to balance a truly conservative estate portfolio. --

As time has passed we can see several major flaws in their thinking. Flaws that cost them a bunch of credibility, if not personal money. [I want to jump in here with a quick quote from Gary North written in 2002:

"I remember in 1975 hearing C. V. Myers tell attendees at a gold conference, 'If you get this one wrong, you'll lose everything.' He was predicting deflation. He got it wrong. He didn't lose everything."

And now back to FOA] One point, that I have touched on here several times, was in understanding just how much ourselves and our economic structure would and did evolve into accepting fiat money use. Even though it was, "god forbid", separated from gold.

In one area alone, the bond markets, investors reacted far differently than deflationists thought they would. Twenty ++ years ago [again, this was written in 2001], it was expected that just gross increases in money printing alone would be enough to crash the bond markets. Not talking about price inflation here, but money inflation and that should have started a deflationary fall in our credit markets. It almost happened, several times, but never followed through. It seemed that the market function had evolved to accept fiat inflation as a prerequisite to modern economic function. In a like comparison to today's thinking; investors assumed that as long as we had an expanding economic stance [nominal GDP growth, credibility inflation and financial product appreciation], sourced by inflating fiat supply, price inflation would not impact long bond credibility. We saw confirmation of this over many years. We saw that our credit markets, especially long bonds, were used in spite of the price inflation threat. Indeed, there was a ready [highly liquid] market demand for bond purchases.

In hind sight, long term holders of bonds did do very well if their position was part of a balanced holding and they didn't need to sell at bad times. Even now, dollar bonds have gained as rates are pushed lower.

Back to the thought:

This whole IMF dollar system has always been based on an expanding fiat theory that swells [nominal] GDP over time. Investors that bet on deflation coming along, after each of our bouts of inflation, were badly burned as deflation was overcome. Economic function returned, essentially because price inflation could not rout the overall market for long credit.

The flaw in all of this was in the reserve structure of our Dollar IMF money system. The fact that the world had to walk, lock step, with our money policy meant that their goods production would almost always be cheaper than ours; keeping local US price inflation under control. In other words; local US-based price inflation could not get out of hand as long as the rest of the world was willing to use their economic production to control it by selling [products cheaper than we could produce them] into our expanding fiat system.

In this, the dollar [and its securities, and their derivatives] could be inflated without end while our credit markets functioned in a non-inflationary environment.

But there is an end.

A money system like this has a definite timeline and that point is reached when the world can move away from keeping price inflation low in the US. That point is reached when Another money system comes along to challenge the dollar and, in the process, offer these other goods-producing countries a chance to buy some "lifestyle" for themselves.

At first, the show is dull as investors keep right on buying into the dollar argument above: that an expanding fiat base builds non-inflationary [nominal] growth [in both GDP and securities]. This is one reason traders still buy US long credit, not to mention chasing rising dollar exchange rates; they expect more of the last several decades of economic theory to keep right on going. It won't.

The dollar faction saw its match early in the 90s as the Euro was taking shape. To counter this threat, as I have outlined here in several ways, they promoted derivative hedges as a way of insuring dollar dominance. These hedges, including gold derivatives, only served to leverage the entire dollar / IMF system beyond its ability to serve as a real fiat money system, today. [See (my title): Is the Fed selling Hyperinflation Insurance Backed Only by Hyperinflation?]

I mean; that our whole dollar landscape has now become just a trading asset arena: it's now evolving away from any meaningful currency use to trade for real goods. It can head in no other direction because our local economic structure, the USA economic base, cannot possibly service even a tiny fraction of the buying power currently held in dollars worldwide.

So what does this have to do with Real estate?

Take a look at any broad section of the US; Northeast, SouthWest, etc.. If any of the deflationists were correct, their reasoning back in the late 70s and early 80s should have produced at least an average fall in Residential real estate. Can any of you find an "average" of property today, that is lower than early 80s prices?

Of course I'm not talking about the spikes in Hawaii, New York, Denver or San Francisco; those are just blips on an ever rising inflation scale. Even if they fall some from here, it isn't part of a deflationary act playing out. Average home prices will rise all across this country no matter what the future economy holds. A super inflationary stance by the Fed means that even unemployed workers can buy a house and pay for it! Watch how this all comes about. The Dow will not be much different when seen ten years from now; a drop to 5,000 then off again, is a real possibility! [Note: The Dow dropped from 11,000 in 2001 down to 7000 and back up to 12,000 in 2011. Again, FOA wrote this ten years ago in 2001]

The same is true for anything perceived as something real: "even silver" (grin).

The difference is in the drastic ups and downs derivatives will place on all asset markets. My point is that we are on an "end time run" in fiat dollar production that will soon produce a spike in real price inflation that crushes hedge vehicles. One item alone, physical gold, because it is the main wealth asset behind the next currency system [See: RPG #1], will outrun everything by a wide margin. No matter the derivative's hold on it!

As the Euro builds a base [which is happening right now in 2011 â see this, this, this, this, this and this], it will drive an inflationary recognition into our credit markets, then freezing up our derivative markets. That perception will fuel a complete failure of our bond markets and force the Fed to buy up any and all credit; paying in full. [Paying full price for deflating assets? Oh my, would the Fed ever do that? The deflationists never saw it coming!] If needed, Bush and congress will see to it that enough money is printed so we are paid in cash for everything! Don't laugh, this is where we are headed.

Gold is $1,581/oz today. When it hits $2,000, it will be up 26.5%. Let's see how long that takes. - De 3/11/2013 - ANSWER: 7 Years, 5 Months

- - - - -

View Replies (1)

»

» You can also:

|

|

|